You’ve spent months building your fintech platform, but one tiny loophole could let hackers steal customer data in seconds, and no one will forgive you for it.

Scary thought, right?

And it’s not just security that keeps you up at night. There’s the ever-shifting maze of regulations, the pressure to design a platform that can actually scale, and the constant fear that a minor mistake could break the user experience.

Building a fintech platform means getting security, reliability, and compliance right at the same time.

It’s a lot like constructing a high-rise building. You need a strong foundation, solid support beams, safety systems on every floor, and strict rules to make sure everything holds up under pressure. Miss any one of those, and you’re in trouble.

In this blog, we’ll walk you through how to build a fintech software platform step by step, from architecture and security to regulatory compliance, so your product is ready for real users, real transactions, and real scrutiny.

So, let’s begin!

What Are Fintech Software Platforms?

Fintech software platforms are like the engine behind all the digital financial services you use every day. They power mobile banking apps, payment systems, lending platforms, investment tools, and insurance apps.

Table of Contents

Without this software, none of those services would be able to:

- process transactions

- manage accounts

- connect with banks

- or protect sensitive financial data

Even though the user experience may look simple, there’s a lot happening behind the scenes. Your platform might be handling thousands of users at once, processing real money in real time, talking to multiple financial institutions, and staying compliant with strict regulations, all simultaneously.

In short, a fintech platform keeps money moving while making sure data stays protected, and regulators stay satisfied.

Types of Fintech Software Platforms

Fintech platforms come in many forms, depending on what problem you’re solving.

Here are some of the most common types you’ll encounter:

- Banking Apps

These apps let users check balances, transfer money, and pay bills. Behind the scenes, your platform manages secure authentication, transaction processing, and real-time updates.

- Payment Processors

Platforms like Stripe or PayPal make sure money moves safely from one account to another. They handle fraud checks, settlements, and compliance so users don’t have to think about it.

- Lending Platforms

Loan and BNPL platforms evaluate risk, approve applications, manage repayments, and protect borrower data, all while meeting financial regulations.

- Insurtech Solutions

Insurance platforms help users compare, buy, and manage policies online. They store sensitive personal information and follow strict industry rules.

No matter the type, every fintech software platform depends on strong architecture, built-in security, and regulatory compliance. Miss any of these, and the platform could fail or get you in serious trouble.

What are the Latest Trends & Market Overview in the Fintech Industry?

Fintech doesn’t slow down, and neither should your platform. As you build or scale in 2026, a few trends directly affect how you design your system.

Let’s break down the biggest ones.

1. Agentic AI & Autonomous Finance

AI is expected to add up to $1 trillion in value to the global banking industry, and for good reason.

We’ve moved past basic chatbots. Today’s agentic AI can think and act independently. Your platform could automatically manage risk, monitor cash flow, or flag suspicious activity without waiting for human input.

Incorporating AI into your platform early allows it to make real-time decisions safely and reliably, giving you a competitive edge.

2. Embedded Finance

By 2026, embedded finance is expected to handle more than $7 trillion in transactions, and you’ve probably used it without even realizing.

What started as a simple “Pay Now” button has grown into full financial features built directly into everyday apps, such as instant credit, in-app insurance, or automated payouts.

Designing your system modularly from the start makes it easy to add new services quickly without slowing performance or creating compliance risks.

3. RegTech & Compliance-as-Code

RegTech, short for Regulatory Technology, helps platforms automate compliance instead of relying on spreadsheets and manual checks. The market is expected to hit $38 billion by 2030, which is a clear sign that old-school methods just don’t cut it anymore.

If you’re still doing KYC, AML, or reporting by hand, you’re leaving room for delays and mistakes. Compliance-as-code fixes that by building the rules straight into your system.

The payoff?

You stay audit-ready, reduce risk, and don’t have to panic every time regulations change.

4. Real-Time Payments & Instant Settlement

Real-time payments are now a $44.5 billion market, and users expect speed by default.

When money moves in seconds instead of days, the pressure on your platform increases. You have less time to detect fraud, reconcile transactions, or fix errors.

Ensuring your infrastructure can handle live transactions and real-time monitoring helps you maintain reliability and trust.

5. Digital-Only Banks & Neobanks

Digital-only banks and neobanks are booming, set to cross $1.66 trillion in market value. If you’re competing here, the expectations are sky-high.

These banks impress with smooth onboarding, personalized features, and niche offerings for freelancers, startups, or global users.

Aligning your backend, security, and compliance layers from day one ensures a seamless, trustworthy experience for users.

Make Your Platform Future-Ready Before Competitors Do

We implement the latest agentic AI, embedded finance, and RegTech to keep you ahead.

Now that you’ve seen the trends shaping fintech in 2026, you can see how they impact the way your platform is built.

In the next section, we’ll look at the core building blocks of a modern fintech platform, showing what it takes to make it functional, secure, and scalable.

What are the Core Building Blocks of a Modern Fintech Platform?

Building a fintech platform is a bit like assembling a really intricate LEGO set. Every piece has to fit perfectly, or the whole thing can wobble, or worse, fall apart.

To make sure your platform is solid, you need to focus on three main areas: architecture, security, and compliance.

1. Architecture & Infrastructure

Architecture is like a blueprint for your platform. It determines how the system handles thousands of users, multiple integrations, and tons of transactions without breaking a sweat.

Many modern fintech platforms use microservices instead of monolithic structures. Microservices let you update parts of the system independently, which makes rolling out new features or fixing bugs much easier.

You’ll also need cloud infrastructure for flexibility and scalability and a solid API layer to connect your platform with banks, payment processors, and other services.

Resilience

Make sure to include backups, failover mechanisms, and disaster recovery plans so your platform stays available even when things go wrong.

2. Built-In Risk Management & Data Protection

Security needs to be part of the platform from the start. Protect data at every step, from login to transaction.

Use encryption, role-based access, and continuous monitoring to catch suspicious activity early. Think of it as a safety net that stops small issues before they reach your users.

3. Compliance Principles

Regulations like PCI DSS, GDPR, and KYC/AML aren’t just boxes to check; they guide how your platform handles sensitive information.

Incorporate compliance early using logging, audits, and automated checks, so you avoid last-minute scrambles and keep risk under control.

Common mistakes teams make here: Skipping resilience planning, treating security as an afterthought, or leaving compliance until the last minute can quickly turn small issues into major problems.

Now that we’ve covered the essentials, here’s how you can actually build your platform, step by step.

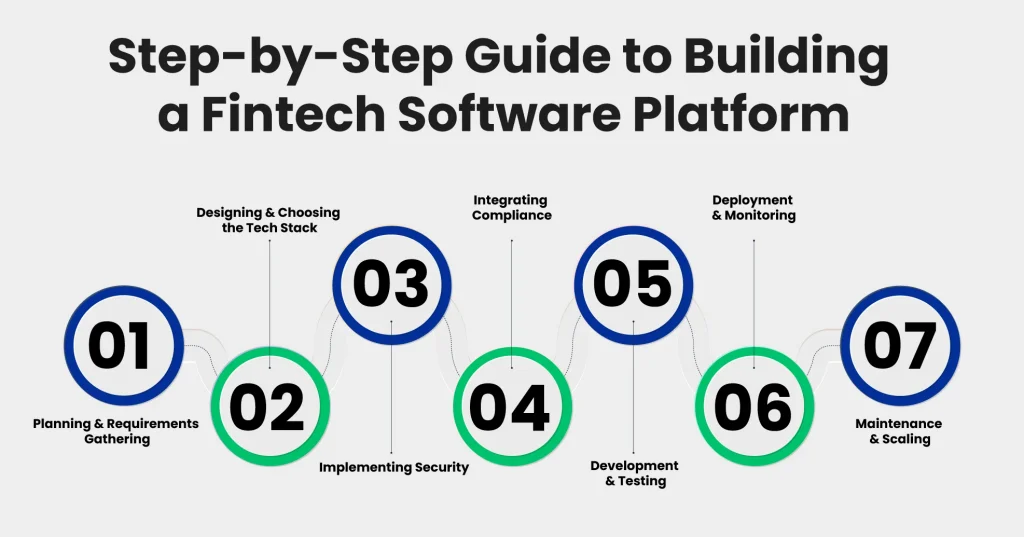

A Step-by-Step Guide to Building a Fintech Software Platform

A fintech platform has a lot to handle at once: architecture, security, compliance, and user experience all demand attention. It can feel overwhelming if you don’t have a clear plan.

In this section, we’ll break everything down into simple, easy-to-follow steps so you know exactly what to do and why.

Step 1: Planning & Requirements Gathering

Before you touch a line of code, get crystal clear on what your platform needs to do:

- Identify Your Users: Are they consumers, small businesses, or enterprises? Each group has different needs.

- Define Core Features: Will you handle payments, loans, in-app insurance, or all three?

- Map Regulatory Requirements: PCI DSS, KYC/AML, and GDPR, and know which rules apply to you from day one.

- Scalability and Performance: Estimate users, transaction volume, and peak loads to plan ahead.

It’s like drawing the map before a road trip; without it, you’re likely to get lost.

Step 2: Designing & Choosing the Tech Stack

This is where your plan becomes a working system. You’re choosing the foundation, materials, and tools that will make your platform functional, scalable, and secure.

| Component | Options | Benefits |

|---|---|---|

| Architecture | Microservices, Monolithic | Determines how your platform scales, maintains stability, and supports updates efficiently. |

| Back-End | Node.js, Python (Django/Flask), Java (Spring Boot) | Handles core platform logic, processes transactions, and supports performance under load. |

| Front-End | React, Angular, Vue.js | Provides responsive, intuitive user interfaces and smooth user experiences. |

| Databases | PostgreSQL, MySQL, MongoDB, DynamoDB | Stores platform data securely and efficiently, supporting both structured and unstructured data. |

| Cloud Infrastructure | AWS, Azure, Google Cloud, Multi-region deployment | Ensures scalable, reliable hosting and compliance with data residency regulations. |

| APIs & Integrations | REST, GraphQL, Third-party integrations | Connects services internally and externally, enabling secure and smooth communication with banks and payment systems. |

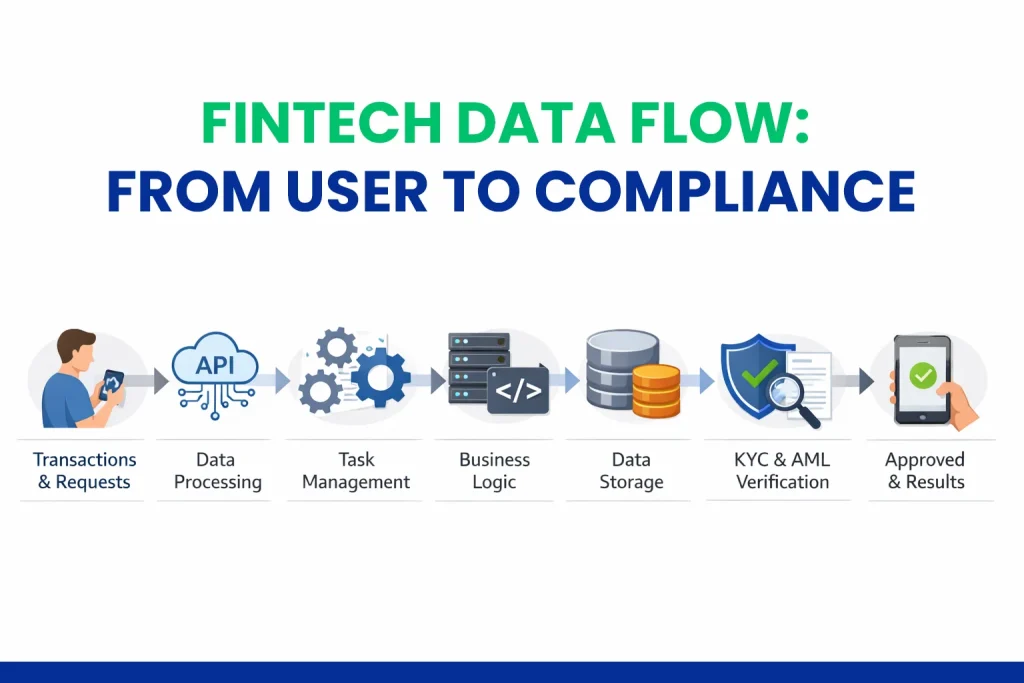

A typical flow looks like this:

Creating a clear, mapped flow highlights bottlenecks, prevents errors, and strengthens security. It also helps your team plan integrations, monitor risks, and implement safeguards before any real-world transactions occur.

Step 3: Implementing Security

Security is non-negotiable. Treat it like locks, cameras, and alarms for your platform:

- Authentication & Authorization: OAuth 2.0, JWT, role-based access control

- Encryption: AES-256 for data at rest; TLS 1.2+ for data in transit

- Fraud Detection: AI/ML models or third-party APIs for suspicious activity

Start with security in mind rather than adding it later; it’s cheaper and safer.

Step 4: Integrating Compliance

Compliance isn’t optional. It should be baked into your platform:

- KYC/AML: Automate identity checks with tools like Jumio or Trulioo.

- PCI DSS: Ensure payments meet industry standards.

- GDPR & Data Residency: Store data in compliant locations.

- Audit & Logging: Automatically log transactions for accountability.

Doing this from the beginning keeps you audit-ready and stress-free.

Step 5: Development & Testing

This is where your plans turn into a working platform. Writing code is exciting, but doing it the right way makes all the difference.

- Agile Sprints: Break development into small, manageable chunks. This way, features roll out steadily, and you can adjust quickly if something isn’t working.

- CI/CD Pipelines: Tools like GitHub Actions, GitLab CI, or Jenkins automate your builds and deployments. Well-designed CI/CD pipelines also help control DevOps cost in fintech by reducing manual effort, deployment failures, and expensive downtime during releases.

- Testing: Use unit tests for individual components, integration tests to check how features work together, and end-to-end tests with Jest, Selenium, or Cypress to make sure everything functions as your users expect.

- Code Reviews: Have teammates review your code to catch bugs, improve security, and share knowledge across the team.

Following these steps ensures your platform runs smoothly, behaves predictably, and keeps user data safe.

Step 6: Deployment & Monitoring

Going live isn’t the finish line; you need to keep a close eye on your platform.

- Deployment: Containerized setups with Docker or orchestration via Kubernetes make it easy to scale your platform and push updates without downtime.

- Monitoring: Tools like Grafana, Prometheus, or New Relic track uptime, performance, and unusual activity. You’ll know instantly if something goes wrong.

- Incident Response: Have clear playbooks ready for outages, security breaches, or critical errors. Quick, well-practiced responses prevent small issues from becoming big problems.

Monitoring continuously and responding quickly keeps your platform stable and trustworthy.

Step 7: Maintenance & Scaling

Your work doesn’t stop after launch. A fintech platform grows and changes with its users, and proactive maintenance is fundamental.

- Regular Updates: Push feature updates, security patches, and bug fixes consistently. It’s better to make small adjustments often than wait for a major overhaul.

- Scaling Microservices & Databases: As user numbers grow, expand your infrastructure so your platform stays fast and reliable.

- Module Upgrades: Update parts of your system without disrupting the whole platform, keeping the user experience smooth.

This is the routine maintenance; small, steady care prevents big problems down the line.

Building a Fintech Platform Alone is Risky.

Let our experts map every step from architecture to compliance so you launch confidently.

Real-World Fintech Applications

Seeing all the steps and trends can feel abstract, so let’s bring it to life with two real-world examples: PayPal and Robinhood. These platforms show how fintech concepts work in practice, securely, at scale, and while staying compliant.

PayPal: The Everyday Payment Powerhouse

If you’ve ever sent money to a friend, paid for something online, or split a dinner bill, there’s a good chance PayPal handled it.

Behind its simple interface, PayPal juggles a ton of moving parts: secure logins, transaction verification, fraud monitoring, and regulatory compliance across dozens of countries.

- Modular architecture: Payments, account management, and security checks run independently, so the platform stays fast even under heavy use.

- Data protection: Strong encryption keeps your financial info safe from prying eyes.

- Compliance automation: Built-in systems make sure every transaction meets PCI DSS and anti-money-laundering rules.

- Smooth user experience: All this happens behind the scenes, letting you send or receive money in seconds with confidence.

Robinhood: Investing Made Simple

Robinhood made investing accessible to millions of people with its mobile-first platform. Users can trade stocks, ETFs, and crypto without ever stepping into a traditional brokerage. But making that simple interface work takes serious engineering.

- Real-time execution: Trades, portfolio updates, and market data streaming happen instantly, so users see accurate results without lag.

- Secure and compliant: Identity verification, two-factor authentication, and fraud detection protect users and keep the platform in line with SEC and FINRA rules.

- API-driven architecture: Smooth integration with financial institutions and market data providers ensures trades execute reliably.

- User-focused design: The tech works behind the scenes so users can focus on investing without worrying about delays or errors.

Both PayPal and Robinhood show how fintech platforms blend architecture, security, and compliance smoothly. They take complex processes that happen in the background and turn them into experiences that feel effortless to users.

How Does Clustox Build Secure & Compliant Fintech Platforms?

With Clustox, you get a trusted fintech solution that works for your users and your business.

Our secure fintech software development services ensure your platform:

- Handles Growth Effortlessly: Modular and API-driven architecture scales as your user base expands.

- Keeps Data and Users Safe: Advanced security measures protect sensitive information from day one.

- Remains Compliant without Stress: Automated compliance for PCI DSS, KYC/AML, and GDPR so you stay audit-ready.

The outcome?

Your fintech software platform runs smoothly, earns user trust, avoids costly compliance issues, and is ready to succeed in the competitive fintech space.

Summary

Fintech platforms are complex, but they don’t have to feel impossible. Throughout this blog, we’ve explored how planning, architecture, security, and compliance all come together to make a platform that works for both users and businesses.

From identifying your audience and mapping core features to choosing a tech stack and implementing automated compliance, each step lays the foundation for a secure, scalable system.

Real-world examples like PayPal and Robinhood show that when everything behind the scenes is handled right, users enjoy seamless experiences without even noticing the complexity.

With the help of experienced software developers, even emerging fintech startups can create platforms that protect sensitive data, scale confidently as demand grows, and stay audit-ready by design.

It stays audit-ready by design and builds user trust every time someone logs in or completes a transaction.

Remember: thoughtful design, continuous monitoring, and proactive maintenance turn a fintech software platform from a concept into a product users rely on day after day.

Frequently Asked Questions (FAQs)

How Much Does It Cost to Build a Compliant Fintech Platform?

The cost depends on complexity, features, and regulatory scope. For most platforms, you should expect higher upfront investment for security, compliance, and audits. However, building compliance early saves you from expensive fixes, delays, and penalties later.

How Long Does It Take to Launch a Fintech Platform?

Timelines vary, but most compliant fintech platforms take 6 to 12 months from planning to launch. If you start with clear requirements and work with experienced developers, you can avoid rework and move forward with fewer roadblocks.

When Should You Involve Compliance in Fintech Development?

You should involve compliance from day one. If you add it later, you risk architectural changes, failed audits, and launch delays. Early compliance planning keeps your platform audit-ready and reduces long-term risk.

Can You Upgrade Security Without Rebuilding the Entire Platform?

Yes, if your platform is designed modularly. With the right architecture, you can improve encryption, authentication, or fraud detection without disrupting core services or user experience.

Stop Stressing Over Security Audits and Compliance Checks.

Partner with Clustox and focus on growth while we handle the technical and legal backbone.